- Commercial activity continues to trend upwards, thanks to positive performance across all business lines, with year-on-year growth of 5.6% in lending volumes and 5.9% in customer funds

- As expected, net interest income was down in the quarter, this together with lower fees and commission income, and one-off costs associated with a new early retirement plan, resulted in profit declining 29.1% year-on-year. The process is expected to deliver gross savings of 40 million euros from 2027 onwards

- Chief Executive Officer, César González-Bueno, stated: “Over the last few years, Banco Sabadell has undergone an extraordinary process of transformation. The model works, the franchise is doing well, and there is a clear and powerful strategy. Under Marc Armengol’s leadership, the Bank will move to the next level”

- Chief Financial Officer, Sergio Palavecino, noted that: “We have a solid balance sheet and are delivering robust, healthy growth, so our future prospects are very bright. All of this adds to the positive message for the markets and shareholders, and the Institution remains committed to delivering profitability of 16% in 2027”

- Profitability, measured by recurrent RoTE, stands at 14.1%, while the bank’s fully-loaded CET1 ratio stands at 13.2%, having generated 32 basis points of capital during the quarter and raised the ratio by 7 basis points after absorbing the one-off costs associated with the early retirement plan

- The bank has completed its sale of TSB for 2.86 billion pounds, generating more than 400 basis points of capital, and it will pay an extraordinary dividend of 50 euro cents per share on 29 May

5 May 2026

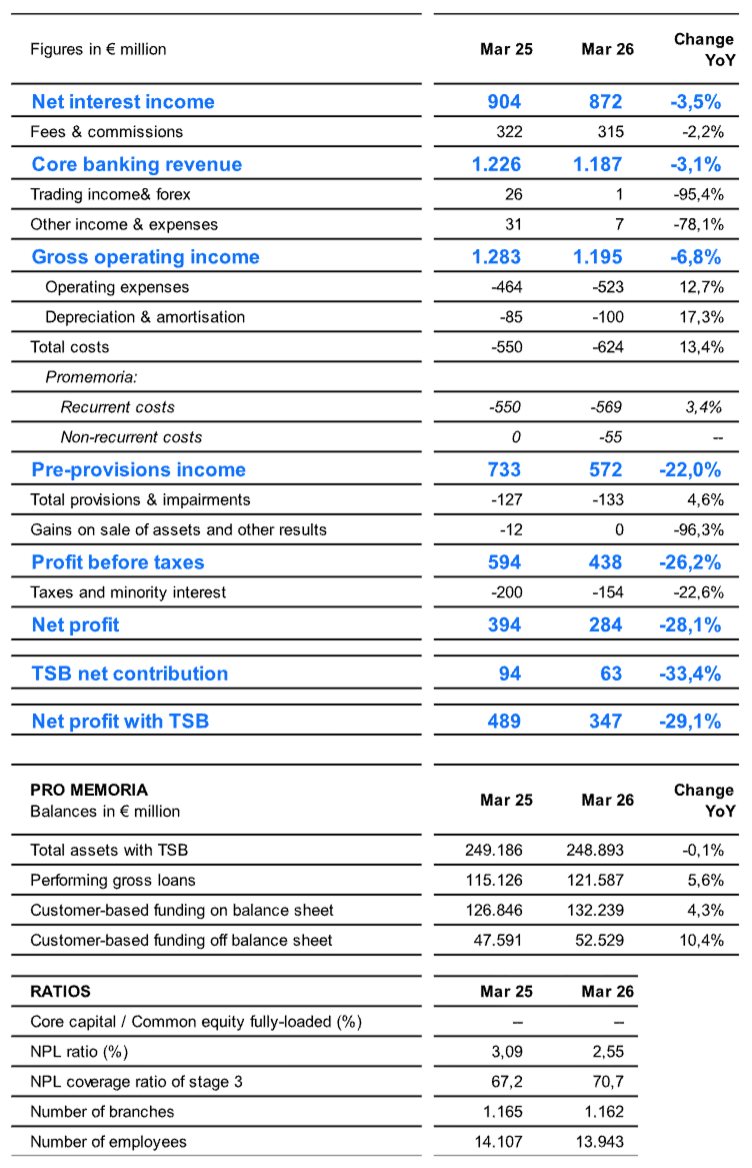

Banco Sabadell Group earned net attributable profit of 347 million euros during the first quarter of 2026, including the net contribution by TSB. This represents a decline of 29.1% less year-on-year, due to non-recurrent costs. These totalled 55 million euros, gross, relating to the new early retirement plan and 14 million euros, gross, due to the sterling hedge linked to the sale of TSB.

The franchise recorded an increase in credit volumes across all segments and also in customer funds, alongside continued improvement in asset quality. These positive trends have partially offset the already anticipated decline in net interest income during the first part of the year, lower fee and commission income during the quarter, and the booking of non-recurrent costs.

The Group’s RoTE rose to 14.1% in recurrent terms, deconsolidating TSB and with no one-off impacts. The Group remains committed to deliver its target of 16% profitability in 2027.

Its solvency ratio, measured as fully-loaded CET1, climbed to 13.2% as at the end of March 2026, having generated 32 basis points of capital during the quarter and raised the ratio by 7 basis points after absorbing the one-off costs associated with the early retirement plan and after deducting the 60% payment rate.

Banco Sabadell’s Chief Executive Officer, César González-Bueno, stated: “In the last few years, Banco Sabadell has undergone an extraordinary process of transformation. The model works, the franchise is doing well, and there is a clear and powerful strategy. Under Marc Armengol’s leadership, the Bank will move to the next level”.

“Our risk profile is good, we are able to generate capital organically, quarter after quarter, whilst still growing in volumes, and our capacity for execution and delivery remains intact. That is why we are keeping our profitability guidance for this year and for the end of the strategic plan, and why we have not changed our shareholder remuneration commitment”, added González-Bueno.

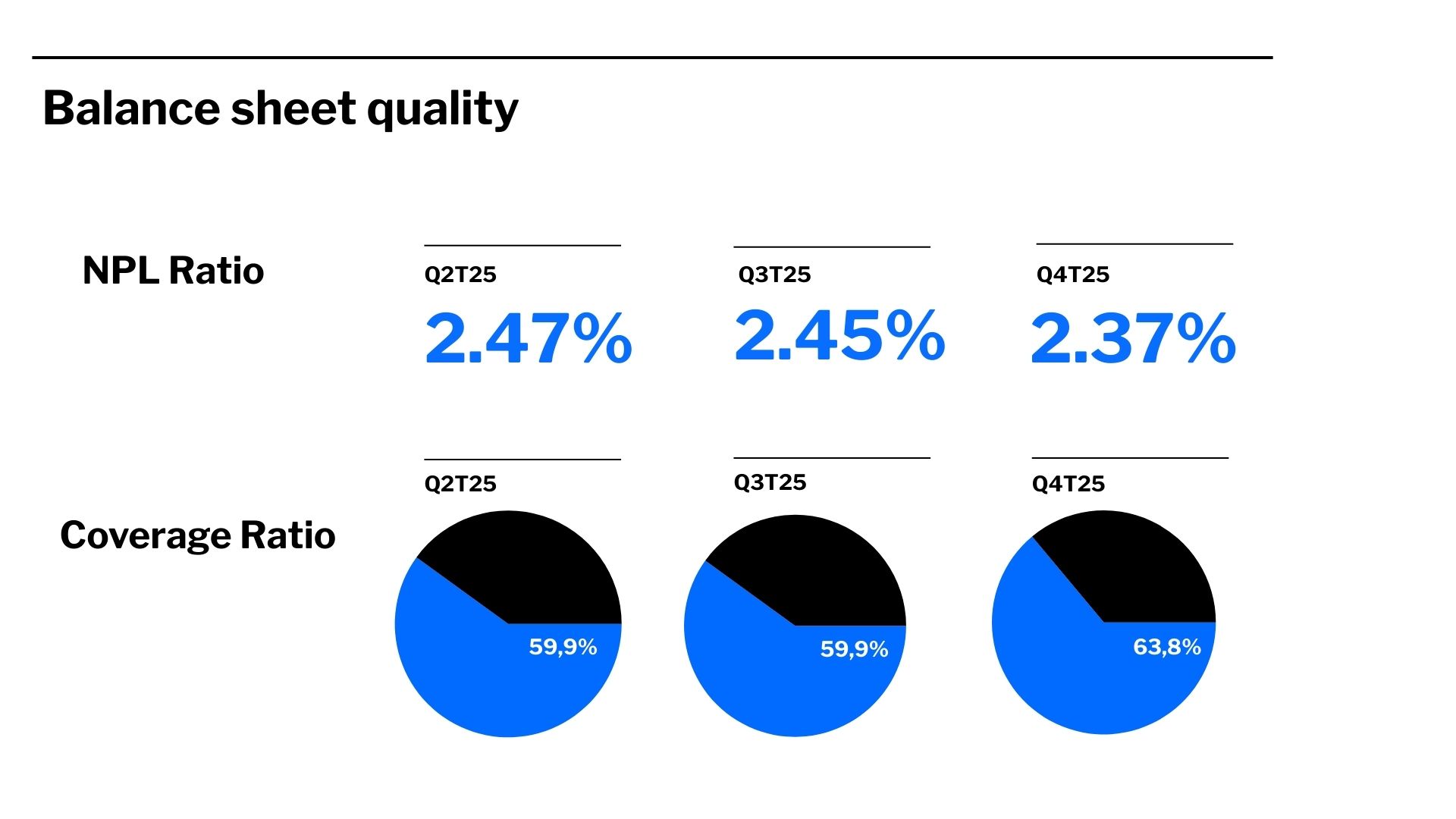

For his part, Chief Financial Officer Sergio Palavecino noted that: “Banco Sabadell is still on track to deliver on its targets and it has considerable and growing financial strength. This is demonstrated both by its ability to generate capital and by the constant improvements in its risk profile, as reflected in the first quarter by the reduction of its NPL ratio, which has fallen to 2.5%, and by its coverage ratio, which has risen to 71%.”

“We have a solid balance sheet and are delivering robust, healthy growth, so our future prospects are very bright. All of this adds to the positive message for the markets and shareholders, and the Institution remains committed to delivering profitability of 16% in 2027”, he added.

Growth in lending volumes and customer funds

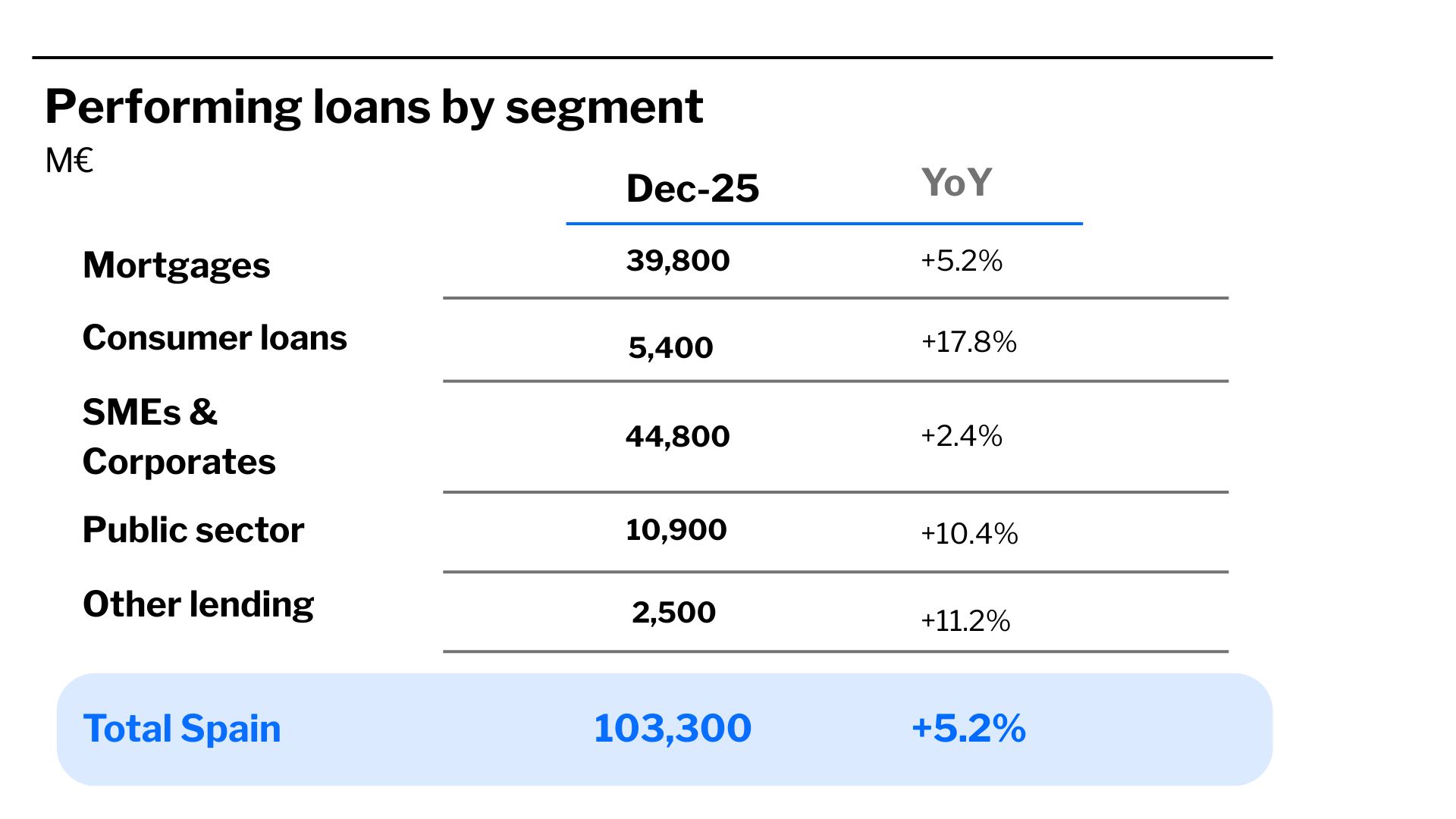

Commercial activity continues its positive trend, driven both by good performance in Spain, which recorded growth across all segments, and by the positive evolution of businesses abroad, in particular Miami and Mexico. Indeed, performing loans ex-TSB, which amounted to 121,587 million euros, recorded year-on-year growth of 5.6% up to March.

In Spain, performing mortgages increased by 4.1% year-on-year to reach 39,800 million euros. Consumer credit increased to 5,500 million euros, which represents total performing portfolio growth of 14.8% year-on-year.

In the segment of loans and credit to SMEs and corporates, the total portfolio grew by 2.1% year-on-year to reach 44,800 million euros. It is worth noting that new long-term loans to SMEs and corporates also picked up by 5% in the quarter, reflecting good market dynamics.

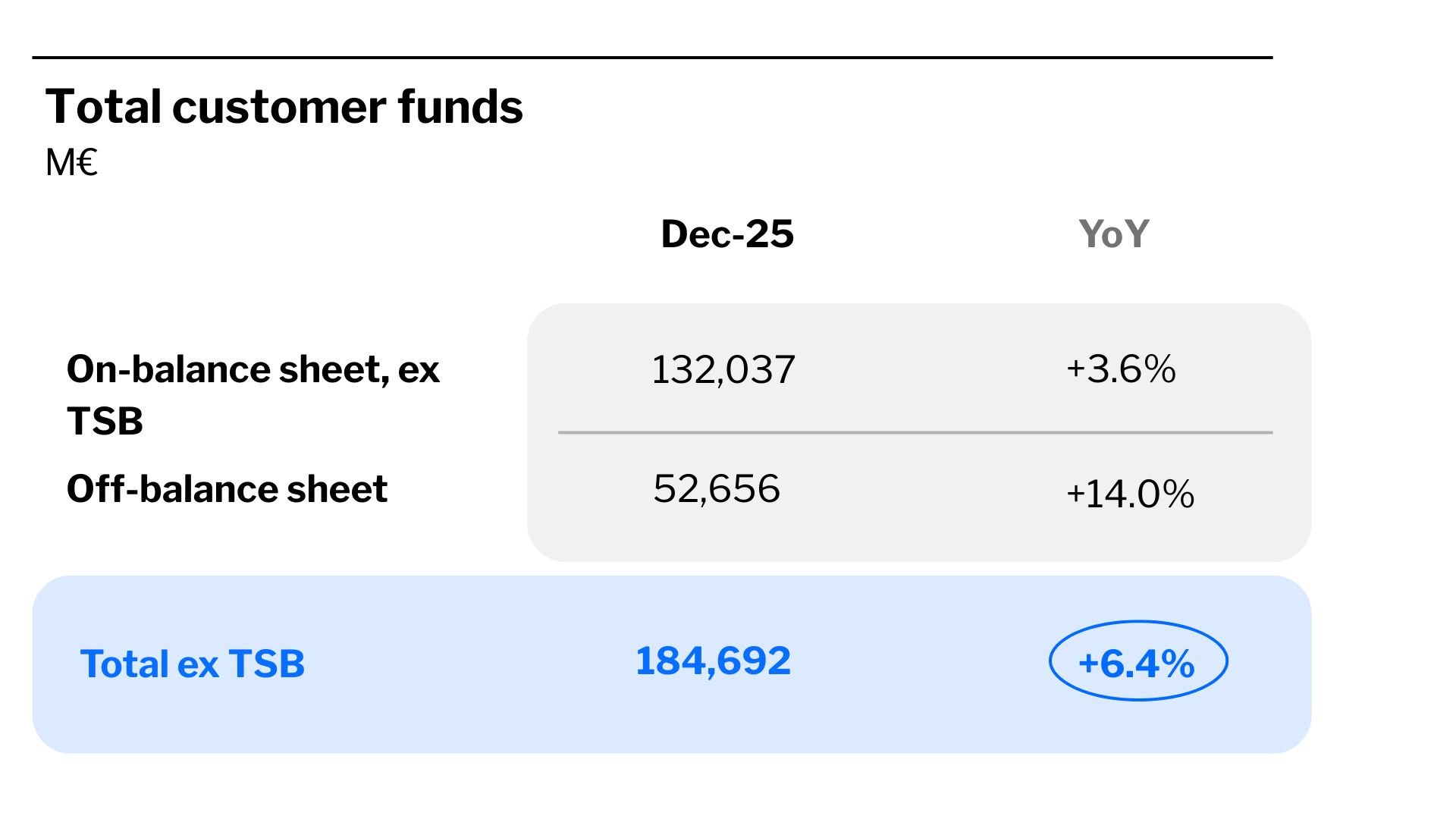

On the liabilities side, total customer funds ex-TSB amounted to 184,768 million euros as at the end of March 2026, representing an increase of 5.9% year-on-year.

On-balance sheet customer funds totalled 132,239 million euros (+4.3% year-on-year), driven by the growth of demand deposit accounts. Off-balance sheet customer funds came to 52,529 million euros (+10.4% year-on-year) as at the end of March, with mutual funds delivering a stand-out performance off the back of positive net subscriptions despite market conditions, alongside positive growth in third-party insurance products and wealth management.

Net interest income is expected to grow with each passing quarter during 2026

In terms of the line items showing profit and loss excluding TSB, Banco Sabadell reported core banking revenue (net interest income plus net fees and commissions) of 1,187 million euros for the first quarter of 2026 (−3.1% year-on-year).

Net interest income reached 872 million euros, representing a year-on-year decline of 3.5%, as expected, due to lower interest rates. Compared to the previous quarter, the decline is 2.5%, affected by the latest negative credit repricing and a lower number of days in the quarter. Banco Sabadell believes that net interest income has bottomed out this quarter and expects to see it follow a steadily improving trend over the rest of 2026, ending the year with growth exceeding 1%, driven by an environment of higher and more volatile interest rates, the growth of business volumes, and a wider customer spread.

Net fees and commissions came to 315 million euros as at the end of March this year, 2.2% lower, due to the smaller contribution of service fees.

Total costs amounted to 624 million euros as at the end of March 2026. Recurrent costs rose by 3.4% year-on-year, mainly due to the increase in depreciation/amortisation and staff expenses, although they were 3% lower than in the previous quarter.

Total costs for the quarter include 55 million euros of non recurring expenses related to the new early retirement plan launched in Spain, which will improve efficiency going forward. Total costs associated with the plan are projected at 90 million euros in 2026, of which 55 million have already been frontloaded in the first quarter. The initiative is expected to deliver annualised gross savings of 40 million euros from 2027 onwards, with one-third of those savings that will already materialise in 2026.

As a result of all the above, the Group’s cost-to-income ratio exTSB, including depreciation and amortisation, reached 52.2% as at the end of March.

In terms of provisions, in the first quarter of 2026 these showed a year-on-year increase of 4.6%, due to the booking of greater credit provisions, which neutralised the reduction in real estate asset provisions, although they remained at contained levels.

With this level of provisions, credit cost of risk stood at 27 basis points as at the end of March 2026 and total cost of risk stood at 38 basis points.

The balance sheet continues to improve

As for balance sheet quality, the NPL ratio ex-TSB fell to 2.55% as at March 2026, from 2.65% as at the end of the previous year, while the stage 3 coverage ratio with total provisions rose to 71%, compared to 69% in the immediately preceding quarter.

This positive evolution of the bank’s default rate reflects the reduction in bank’s non-performing assets, which fell by 106 million euros in the quarter, with loans classified as stage 3 down by 80 million euros and non-performing real estate assets down by 26 million euros.

Over the past twelve months, the bank’s non-performing assets have fallen by 685 million euros, 532 million euros of which correspond to stage 3 loans and the remaining 153 million euros corresponding to distressed real estate assets.

The Group continues to generate capital on a recurring and organic basis at good pace. The fully-loaded CET1 ratio stood at 13.2% at the end of March 2026, with 32 basis points of capital generated during the quarter. The ratio increased by 7 basis points after absorbing one-off costs associated with the early retirement plan and after deducting the 60% payment rate. The ongoing improvement in Banco Sabadell’s solvency is also reflected in the latest assessment of its credit profile by the main credit rating agencies.

As previously announced, with the sale of TSB complete, Banco Sabadell will pay out an extraordinary dividend of 50 euro cents per share on 29 May. The final price of the transaction has risen to 2.86 billion pounds, generating 405 basis points of capital.